Guest Features

Scared about savings and retirement funds? “Stay strong,” says local expert

A little over ten years ago I sat in a meeting during the middle of the financial crisis we now call “The Great Recession,” The speaker was a respected leader in the community who had the ear and trust of those in attendance. At this meeting, he spoke about the severe decline of financial markets and told us that he had sold everything in his company’s retirement plan and suggested that was a prudent thing to do. He was not a financial advisor and to my knowledge had no more experience with personal finances than anyone else in attendance. Fortunately, I did not follow his counsel in an area that was not his expertise.

Markets bottomed in March of 2009 at a broad decline of over 50% from their peak less than a year earlier. We sometimes forget that when markets were already down 50%, fear was reaching a crescendo which made it appear that a dive over the cliff with the remaining value of those portfolios was imminent. By definition – the scariest time to stay invested is when markets bottom. I remember those dark days well as I empathized with frustrated and despondent clients and struggled daily to convince people to stay the course despite the gut-wrenching decline. There was legitimate concern in both individual and institutional investors that the world’s financial systems were broken. For those who were close to retirement or who had recently retired – the situation seemed their worse financial nightmare.

First of all, it is important to point out that markets bottom before economic activity improves. Markets are a discounting machine – looking far into the future for signs of economic activity and responding to those inputs by pricing them in. Markets bottomed in early March 2009 despite the economy not bottoming for months after. What happened after that bottom? In 2009 the market returns were in the high 20% to high 30% depending on how your portfolio was allocated. If you missed that because 2008 and early 2009 scared you into selling, you watched on the sidelines with the knowledge that by selling you had locked in those scary prices and missed the subsequent recovery in prices. I have met many of these people over the last ten plus years and for many of them, their financial lives and plans for their future have never recovered. Their understandable fear led them to behavior (selling) that they regretted ever since.

With that as a backdrop, I write this column with markets down ~30% from their peak levels a little less than a month ago. Declines have been driven by fears and uncertainty on Covid-19 and a simultaneous oil production fight between Saudi Arabia and Russia. The fear, uncertainty, and questions I am hearing now are reminiscent of those from late 2008 and 2009.

The permanent and most troubling impact of Covid-19 will likely be high death rates for seniors and those with pre-existing health conditions who contract the virus. The best data now indicates that unless we are very fortunate, these rates will be far more serious (7-10X +) what we generally see in annual flu deaths. To avoid this and perhaps spread the impact on the health care system we are encouraged to exercise “social distancing.” While this will hopefully reduce deaths caused by the virus it will also have a significant economic impact by shutting down much of the regular commerce and travel that is so important to our economic system. Let me be clear – the economic impact of Covid-19 will be substantial in the short run – including a probable worldwide recession in the quarters to come. However, unlike previous downturns, there is light at the end of the tunnel and even a time frame for expecting that recovery. We know that the virus will run its course over the next couple of months and that economic activity will return to its normal levels – including going out to eat, air travel, cruises, and road trips.

What to do? Decisions on investing which should have included discussions of risk tolerance and asset allocations are generally decided dispassionately. Any decisions made in the middle of a crisis are by definition driven by fear and frustration and are therefore not likely to be driven by data.

My suggestions to those of you who are fearing for your financial future:

• If you do not have an experienced, cool-headed fiduciary financial advisor (one not paid through commissions) – get one. You will find their experience and commitment to your best interest invaluable as you navigate the next six months.

• Decisions made dispassionately with data are preferential to those based on emotions. Stay the course. If you do not need to use the bulk of the invested money in the next couple of years, there is no reason to sell. If fact, this may be a great opportunity if you have dry powder and the nerve to put it to work when others are paralyzed by fear

• If possible, limit the distributions you take from your investment accounts during the downturn. Distributions made during severe declines can significantly reduce the value of your portfolios once they recover.

• Don’t treat financial markets like a casino. If you are “playing” with individual stocks you are likely to be burned when something negative happens to their price and you lose your nerve.

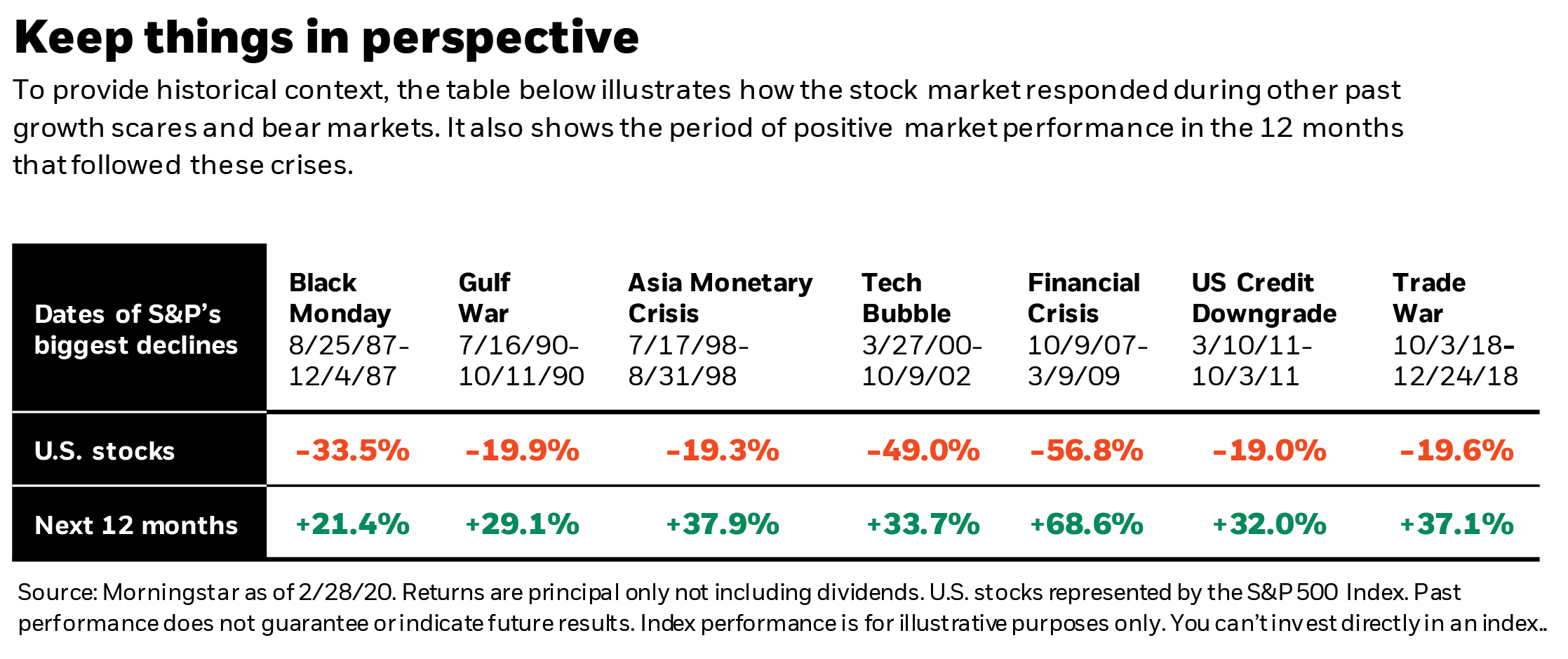

• Look past the current declines to a better future for your investments. Markets have historically produced prodigious returns after severe declines. The average time to regain previous highs is 24 months from the trough. (see graphic)

Mike Johnson is the Founder and President of Pillar Capital, a Lehi based Registered Investment Advisor. He can be reached at 801-770-3301 or mike@pillarcapital.com.

{kind=link}